Questions to consider:

- What simple steps do I take to create a financial plan?

- How do I use financial planning in everyday life?

- How is the financial planning process implemented for every purchase?

If you fail to plan, you are planning to fail.

Honestly, practicing money management isn’t that hard to figure out. In many ways it’s similar to playing a video game. The first time you play a game, you may feel awkward or have the lowest score. Playing for a while can make you OK at the game. But if you learn the rules of the game, figure out how to best use each tool in the game, read strategy guides from experts, and practice, you can get really good at it.

Money management is the same. It’s not enough to “figure it out as you go.” If you want to get good at managing your money, you must treat money like you treat your favorite game. You have to come at it with a well-researched plan. Research has shown that people with stronger finances are healthier1 and happier,2 have better marriages,3 and even have better cognitive functioning.4

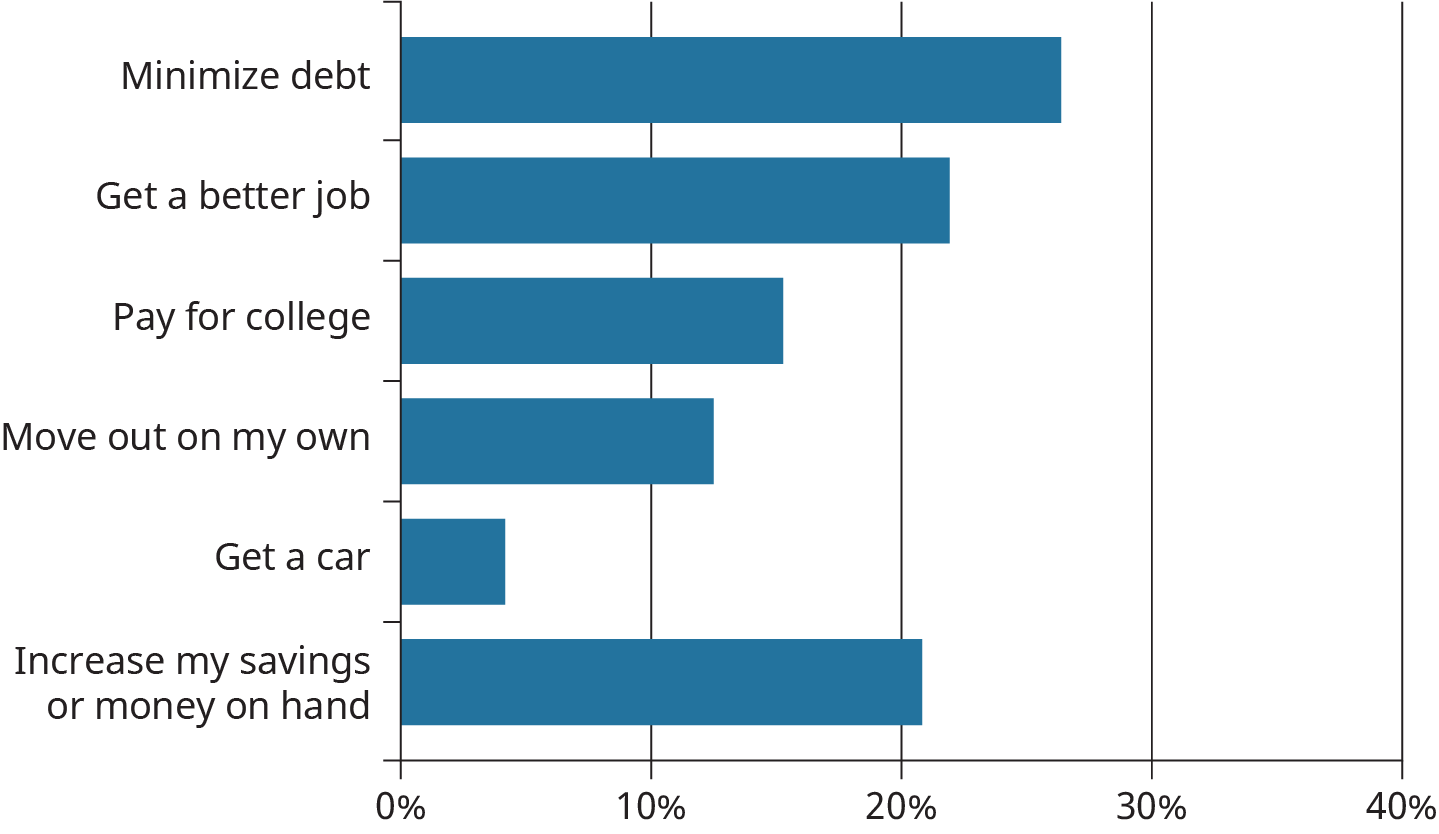

- What is your top immediate financial priority?

- Minimizing debt

- Get a better job

- Pay for college

- Move out on my own

- Get a car

- Increase my savings or money on hand

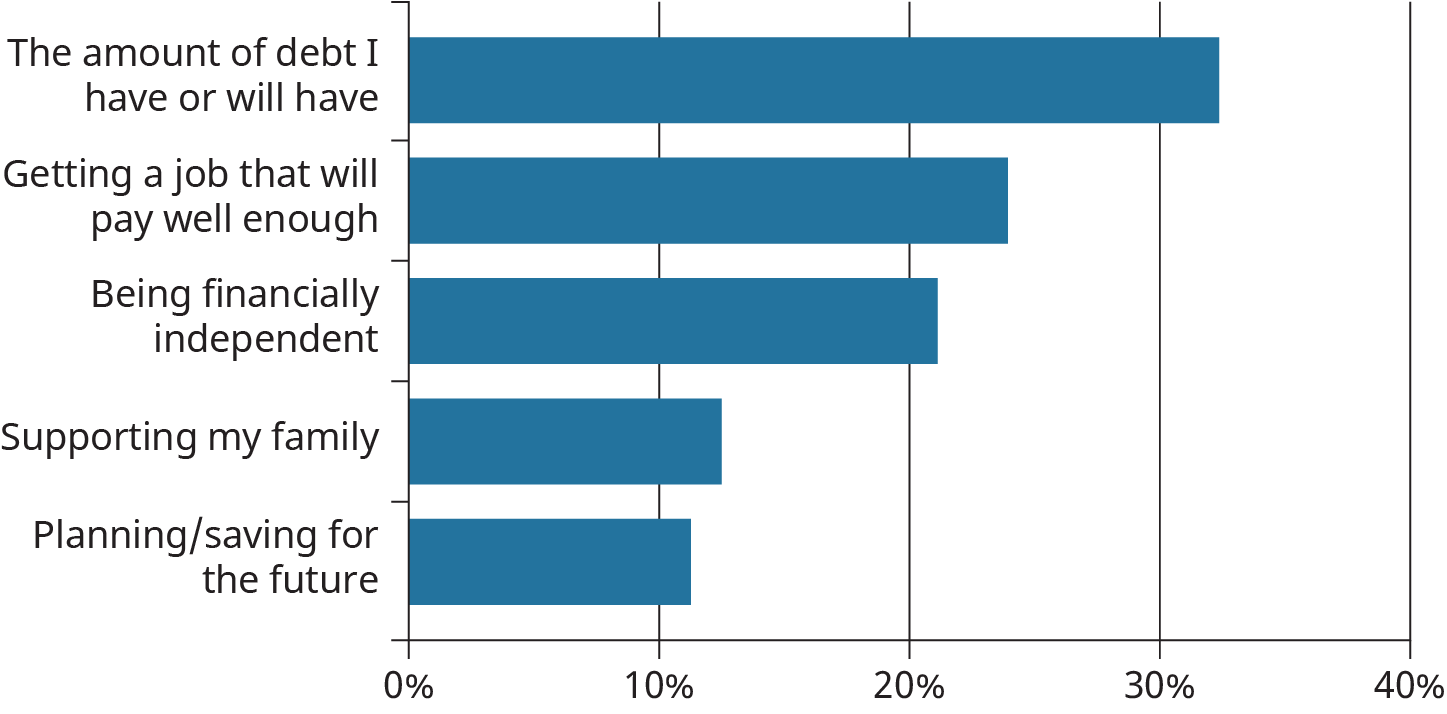

- Which aspect of your finances concerns you the most?

- The amount of debt I have or will have

- Getting a job that will pay well enough

- Being financially independent

- Supporting my family

- Planning/saving for the future

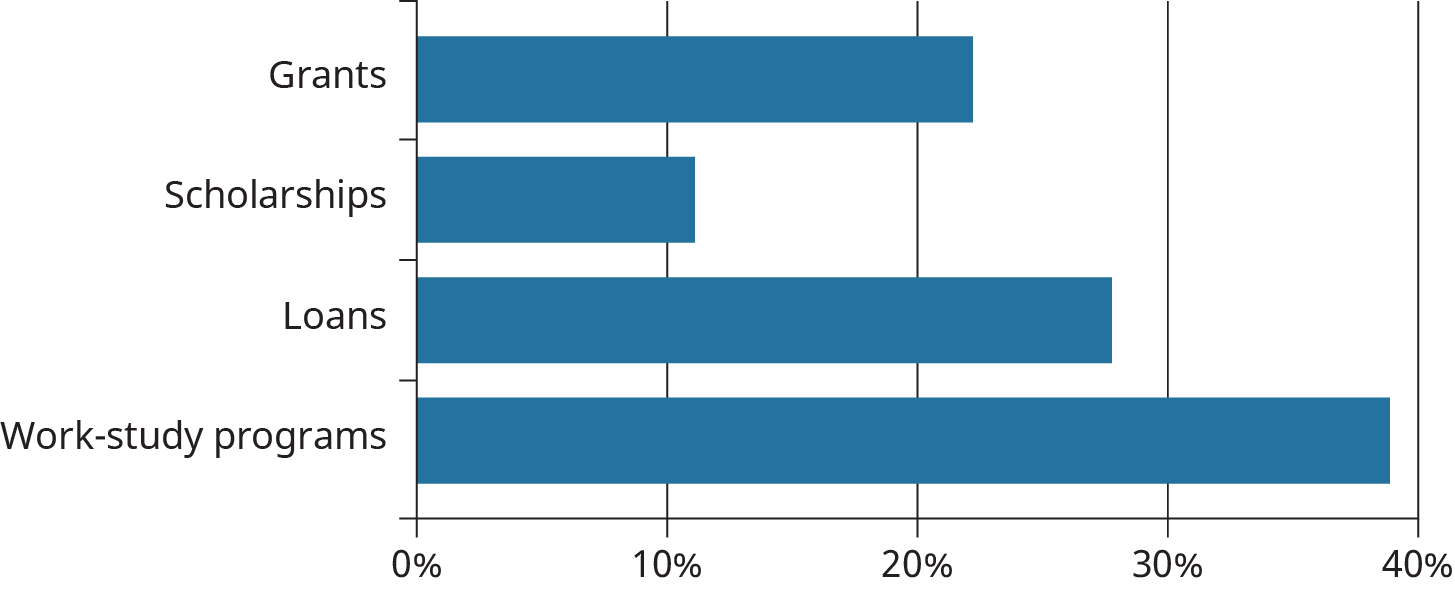

- When considering how to pay for college, which of the following do you know least about?

- Grants

- Scholarships

- Loans

- Work-study programs

You can also take the anonymous What Students Say Survey below.

Students offered their views on these questions, and the results are displayed in the graphs below.

What is your top immediate financial priority?

Which aspect of your finances concerns you the most?

Which aspect of your finances concerns you the most?

When considering how to pay for college, which of the following do you know least about?

When considering how to pay for college, which of the following do you know least about?

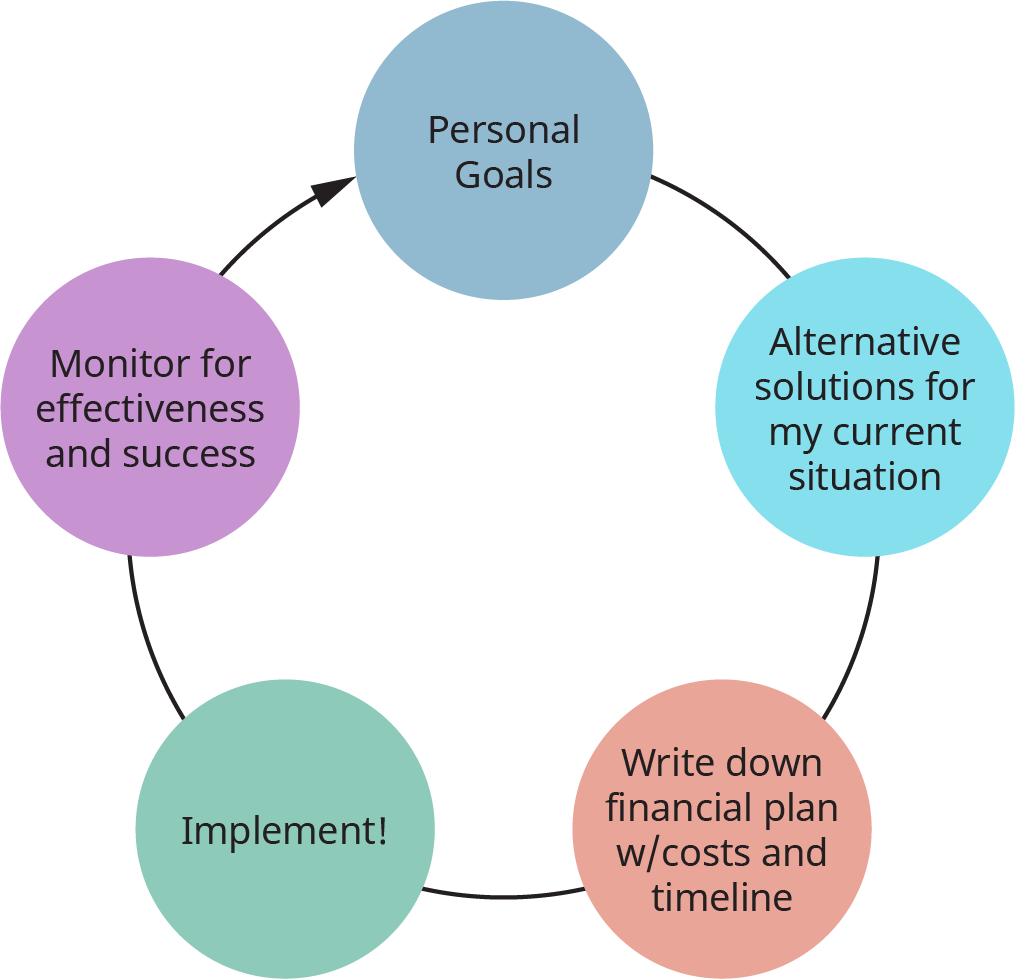

Financial Planning Process

Personal goals and behaviors have a financial component or consequence. To make the most of your financial resources, you need to do some financial planning. The financial planning process consists of five distinct steps: goal setting, evaluating, planning, implementing, and monitoring. You can read in more depth about SMART goals in chapter 3.

Financial Planning in Five Steps

- Develop Personal Goals

- What do I want my life to look like?

- Identify and Evaluate Alternatives for Achieving Goals for My Situation

- What do my savings, debt, income, and expenses look like?

- What creative ways are available to get the life I want?

- Write My Financial Plan

- What small steps can I take to start working toward my goals?

- Implement the Plan

- Begin taking those steps, even if I can only do a few small things each week.

- Monitor and Adjust the Plan

- Make sure I don’t get distracted by life. Keep taking those small steps each week. Make adjustments when needed.

How to Use Financial Planning in Everyday Life

The financial planning process isn’t only about creating one big financial plan. You can also use it to get a better deal when you buy a car or computer or rent an apartment. In fact, anytime you are thinking about spending a lot of money, you can use the financial planning process to pay less and get more.

To explore financial planning in-depth, we’ll use the example of buying a car.

1. Develop Goals

First, what do you really need? If you’re looking for a car, you probably need transportation. Before you decide to buy a car, consider alternatives to buying a car. Could you take a bus, walk, or bike instead? Often one goal can impact another goal. Cars are typically not good financial investments. We have cars for convenience and necessity, to earn an income and, to enjoy life. Financially, they are an expense. They lose value, or depreciate, rather than increasing in value, like savings. So buying a car may slow your savings or retirement plan goals. Cars continually use up cash for gas, repairs, taxes, parking, and so on. Keep this in mind throughout the planning process.

2. Identify and Evaluate Alternatives for Achieving Goals in Your Current Situation.

For this example, let’s assume that you have determined the best alternative is to buy a car. Do you need a new car? Will your current car last with some upkeep? Consider a used car over a new one. On average, a new car will lose one-fifth of its value during its first year.5 Buying a one-year-old car is like getting a practically new car for a 20 percent discount. So in many cases, the best deal may be to buy a five- or six-year-old car. Sites such as the Kelley Blue Book website (KBB.com) and Edmunds.com can show you depreciation tables for the cars you are considering. Perhaps someone in your family has a car they will sell you at a discount.

Do you know how much it will cost in total to own the car? It will help to check out the total cost of ownership tools (also on KBB.com and Edmunds.com) to estimate how much each car will cost you in maintenance, repairs, gas, and insurance. A cheap car that gets poor gas mileage and breaks down all the time will actually cost you more in the long run.

3. Write Down Your Financial Plan

| Goal | Item | Details | Budget | Timeline |

|---|---|---|---|---|

| Transportation/Car | 2014 Toyota Camry | Black, A/C, power windows, less than 60,000 miles |

Car $12,000 (max) Down payment $3,000 Insurance $100/mo Sales tax $900 + Licensing $145 Cash needed $4,145 |

Have $3600 in savings for this. Save $50/week. Purchase in approximately 11 weeks. |

| Computer | Used or refurbished laptop | Dell w/ Windows, minimum 13″, 128G hard drive, HD Graphics |

$300 Use free Windows update from school. Use free Wi-Fi at school. |

Sell current laptop for $100. Buy refurbished from Dell site for $289. $189 on credit card. Pay off when statement comes. |

Examples of financial plans for a car and a computer.

4. Implement Your Plan

Once you’ve narrowed down which car you are looking for, do more online research with resources such as Kelley Blue Book to see what is for sale in your area. You can also begin contacting dealerships and asking them if they have the car you are looking for with the features you want. Ask the dealerships with the car you want to give you their best offer, then compare their price to your researched price. You may have to spend more time looking at other dealerships to compare offers, but one goal of online research is to save time and avoid driving from place to place if possible.

When you do go to buy the car, bring a copy of your written plan into the dealership and stick to it. If a dealership tries to switch you to a more expensive option, just say no, or you can leave to go to another dealership. Remember Elan in our opening scenario? He went shopping alone and caved to the pressure and persuasion of the salesperson. If you feel it is helpful, take a responsible friend or family member with you for support.

5. Monitor and Adjust the Plan to Changing Circumstances and New Life Goals

Life changes and things wear out. Keep up the recommended maintenance on the car (or any other purchase). Keep saving money for your emergency fund, then for your next car. The worst time to buy a car is when your current car breaks down because you are easier to take advantage of when you are desperate. When your car starts giving you trouble or your life circumstances start to change, you will be ready to shop smart again.

A good practice is to keep making car payments once the car loan is paid off. If you are paying $300 per month for a car loan, when the loan is paid off, put $300 per month into a savings account for a new car instead. Do it long enough and you can buy your next car using your own money!

Use the Financial Planning Process for Everything

The same process can be used to make every major purchase in your life. When you rent an apartment, begin with the same assessment of your current financial situation, what you need in an apartment, and what goals it will impact or fulfill. Then look for an apartment using a written plan to avoid being sold on a more expensive place than you want.

You can even use the process of assessing and planning for small things such as buying textbooks or weekly groceries. While saving a few bucks each week may seem like a small deal, you will gain practice using the financial planning process, so it will become automatic for when you make the big decisions in life. Stick to your plan.

Footnotes

- 1 https://www.sciencedirect.com/science/article/pii/S0277953613002839

- 2 https://academic.oup.com/geronj/article-abstract/38/5/626/578092

- 3 https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1741-3729.2012.00715.x and http://onlinelibrary.wiley.com/doi/10.1111/j.1741-3729.2012.00715.x/abstract

- 4 https://science.sciencemag.org/content/341/6149/976%20

- 5 Krome, Charles. “Car Depreciation.” 2018, Carfax. https://www.carfax.com/blog/car-depreciation

Source: OpenStax College Success is licensed under Creative Commons Attribution License v4.0